Page 167 - Pakistan Oilfields Limited - Annual Report 2021

P. 167

NOTES TO AND FORMING

PART OF THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2021

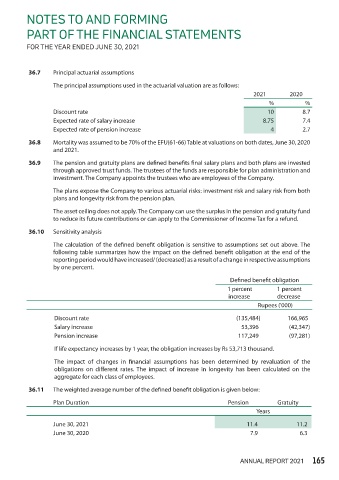

36.7 Principal actuarial assumptions

The principal assumptions used in the actuarial valuation are as follows:

2021 2020

% %

Discount rate 10 8.7

Expected rate of salary increase 8.75 7.4

Expected rate of pension increase 4 2.7

36.8 Mortality was assumed to be 70% of the EFU(61-66) Table at valuations on both dates, June 30, 2020

and 2021.

36.9 The pension and gratuity plans are defined benefits final salary plans and both plans are invested

through approved trust funds. The trustees of the funds are responsible for plan administration and

investment. The Company appoints the trustees who are employees of the Company.

The plans expose the Company to various actuarial risks: investment risk and salary risk from both

plans and longevity risk from the pension plan.

The asset ceiling does not apply. The Company can use the surplus in the pension and gratuity fund

to reduce its future contributions or can apply to the Commissioner of Income Tax for a refund.

36.10 Sensitivity analysis

The calculation of the defined benefit obligation is sensitive to assumptions set out above. The

following table summarizes how the impact on the defined benefit obligation at the end of the

reporting period would have increased/ (decreased) as a result of a change in respective assumptions

by one percent.

Defined benefit obligation

1 percent 1 percent

increase decrease

Rupees ('000)

Discount rate (135,484) 166,965

Salary increase 53,396 (42,347)

Pension increase 117,249 (97,281)

If life expectancy increases by 1 year, the obligation increases by Rs 53,713 thousand.

The impact of changes in financial assumptions has been determined by revaluation of the

obligations on different rates. The impact of increase in longevity has been calculated on the

aggregate for each class of employees.

36.11 The weighted average number of the defined benefit obligation is given below:

Plan Duration Pension Gratuity

Years

June 30, 2021 11.4 11.2

June 30, 2020 7.9 6.3

ANNUAL REPORT 2021 165